An economic and usage analysis of utility consumption in the tri-state region as well as the potential impact of regulation on prices for residential consumers.

Published July 1, 2001

By Allison L. C. de Cerreño, Ph.D., Mahmud Farooque, and Veronica Hendrickson

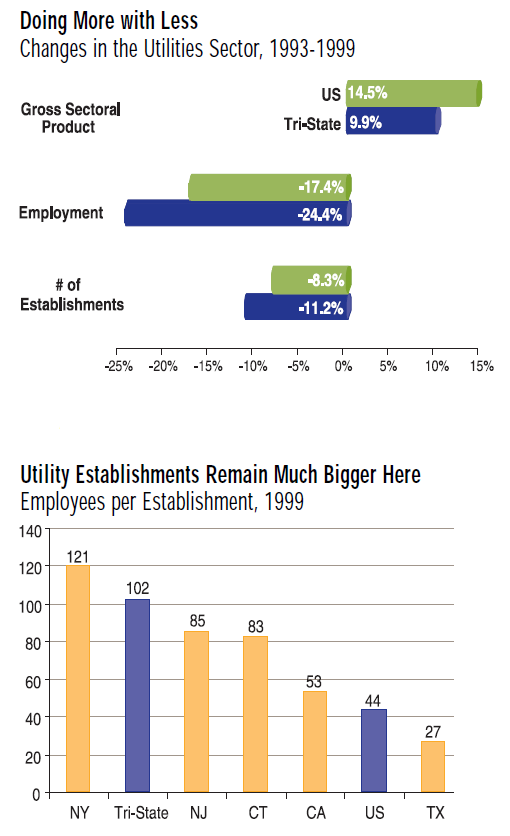

Energy supply is not all that has become scarce in the utilities industry. There are fewer establishments and even fewer employees than there were a decade ago. In spite of this tapering of the labor market, sectoral output in the United States has gone up steadily, increasing by close to 15% between 1993 and 1999. The Tri-State region has followed the national pattern in reduction of workforce and rise in output. However, sectoral product grew rather slowly while there was a sharper decline in the employment base.

The greater loss in jobs is partly due to the fact that establishments in the region are larger than other parts of the country. Although the NY/NJ/CT region represented only 5% of the nation’s utility establishments in 1999, it accounted for 11% of the total employment and 13% of the annual payroll. Utility establishments in the Tri-State region employ on average nearly twice as many people as their counterparts in California; nearly four times as many as in Texas.

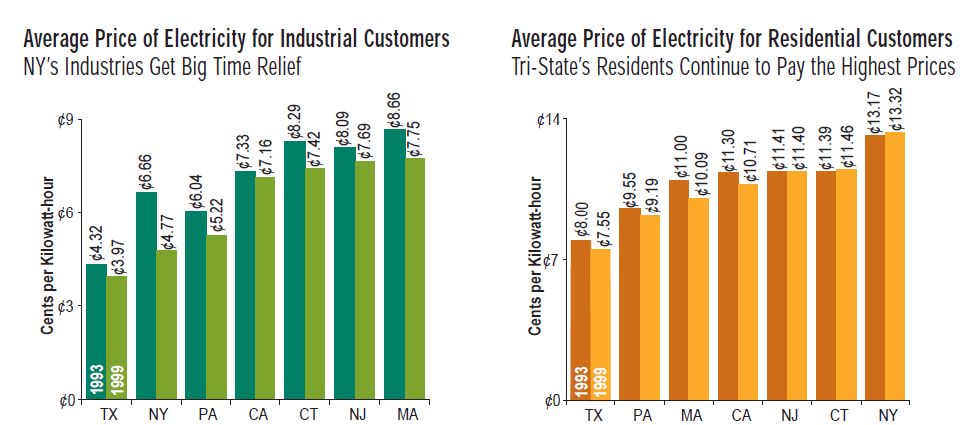

Unbundling of the electric utilities in the 1990s has made the sector more efficient and productive. However, unlike the cases in the airline and telecommunication industries, deregulation is yet to bring a dramatic reduction in the price of electricity, especially for residential customers

Water Utilities: Projections are Up, but Who Will Pay?

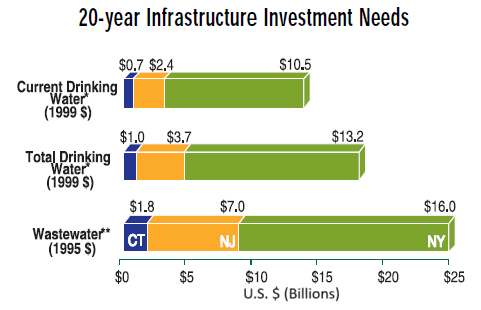

New regulation and improved technology have produced the opposite effect on the region’s employment in the water supply and sanitary services industries. An increase in the number of contaminants that must be monitored and treated has prompted the Bureau of Labor Statistics to project a 34% increase in employment between 1998 and 2008. However, the price tag for required maintenance and regulatory compliance for the region is hefty: about $25 billion for wastewater and $18 billion for drinking water, accounting for 18% and 13% of the United States’ totals respectively.

Energy Consumption in the Tri-State Region

Efficient

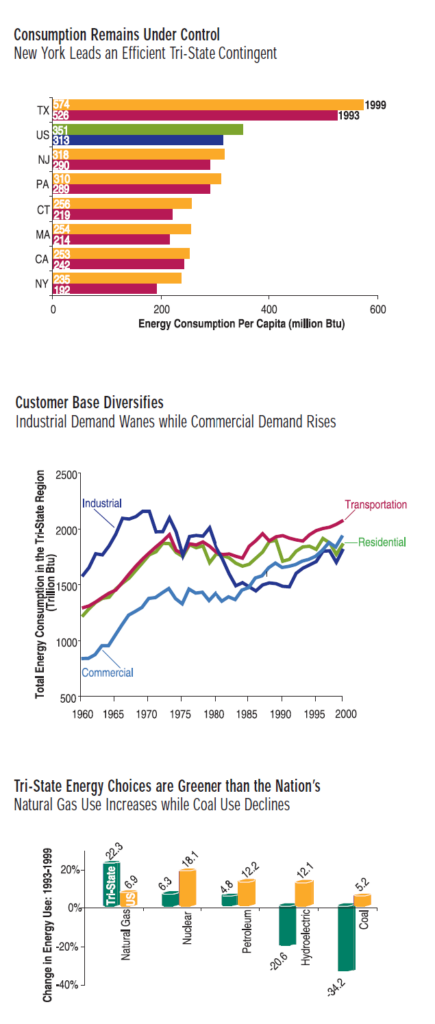

In 1999, 14% of the nation’s population resided in the NY/NJ/CT region but accounted for only 8% of the U.S.’s total energy consumption, a rather significant difference. Without the region, per capita energy consumption in the country would increase by more than 3%. Had the Tri-State region’s population consumed energy at the same rate as the rest of the U.S., the total energy usage would have increased by 3010 trillion Btu – more than the total energy consumed in Georgia that year.

Balanced…

Nationally, industrial demand led all other sectors in terms of energy consumption, accounting for 37% of the total energy consumed in 1999. Commercial demand, at 16% of the total, was the lowest of all four sectors. The pattern is similar to that of the Tri- State region, but some thirty years ago. Industrial sector’s share of the total energy pie has been decreasing steadily in the region. Today, each of the four sectors (industrial, commercial, residential and transportation) consumes about a quarter of the total energy.

However, these shifts have not been uniformly distributed across the region. For example, between 1993 and 1999, industrial demand in NY and CT rose by 23% and 5% respectively, but in NJ it dropped by 2%. This loss in industrial demand for energy was more than compensated by a 2.6% increase in the residential sector in a period when New Jersey saw its resident population increase by 3.4%.

And Environment-Friendly…

Coal provided 20% of the region’s total energy in 1960, a share that dropped to just 3% in 1999. Nationally, consumption of coal continued to hover around the 20% mark, remaining essentially unchanged in the last four decades. Share of natural gas in the NY/NJ/CT region doubled, while nationally, it experienced a 4% decrease from its 1960 levels. Nearly 83% of the total energy consumed in the U.S. came from just three sources: petroleum, natural gas and coal. By contrast, these three accounted for 73% of the total energy consumed in the region, with the remainder coming from hydroelectricity, nuclear, and other sources.

Also read: New York’s Power Woes and Deregulation’s Impact

Sources

- United States Census Bureau, County Business Patterns, 1993-1999

- United States Department of Commerce, Bureau of Economic Analysis, Gross State Product Data, 1993-1999.

- United States Census Bureau, County Business Patterns, 1993-1999.

- United States Environmental Protection Agency, 1999 Drinking Water Infrastructure Needs Survey.

- United States Environmental Protection Agency, 1996 Clean Water Needs Survey.

- United States Department of Energy, Energy Information Administration, State Energy Data Report, 1999.